This article is a part of Poland Unpacked. Weekly intelligence for decision-makers

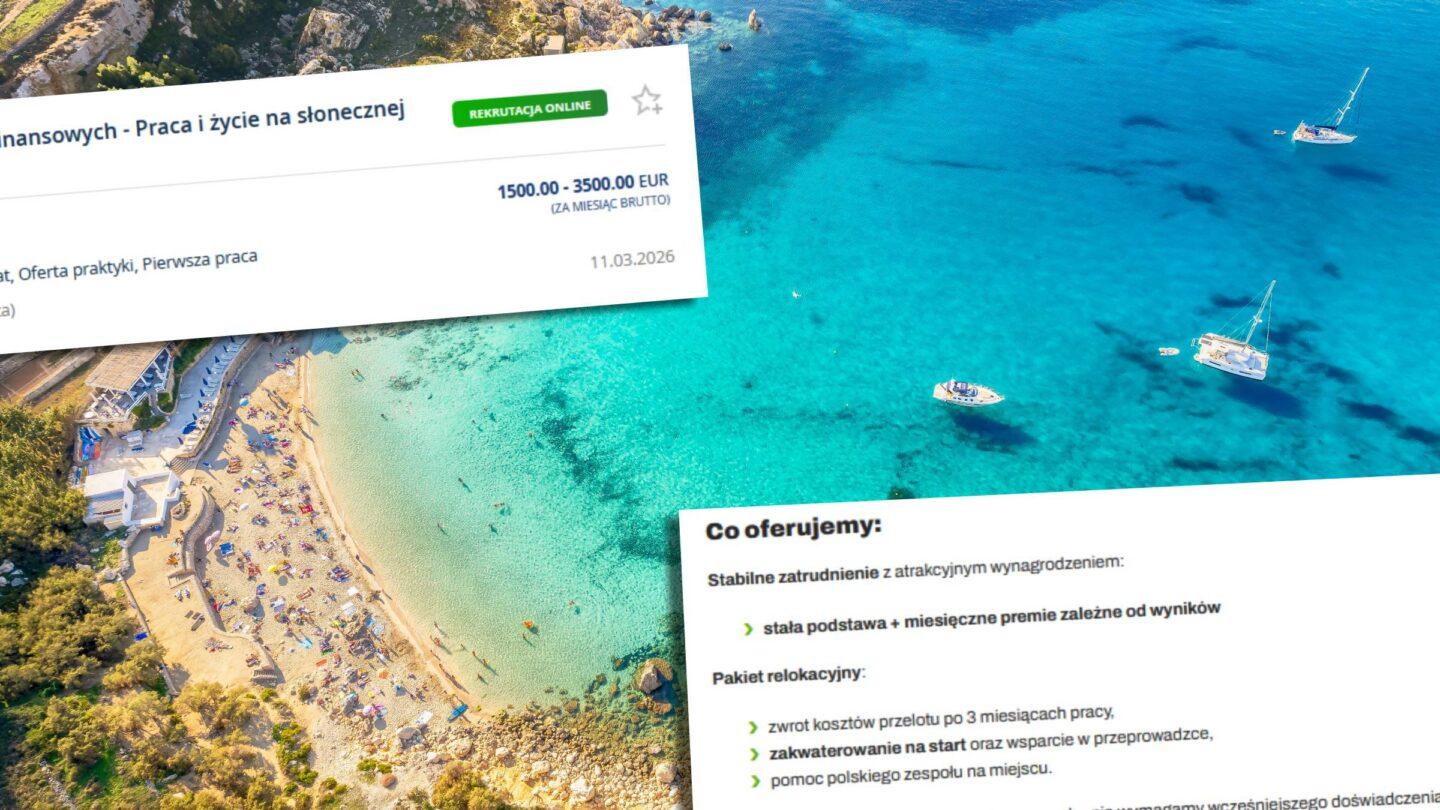

In job ads by GCC7 targeting Poles, candidates are tempted with salaries of up to PLN 15,000 gross (approx. EUR 3,500) – no experience required, plus relocation to Malta, a “Mediterranean paradise” with 350 days of sunshine a year. Yet, as one source tells XYZ, once on the island a new hire quickly discovers what the job really entails: their task is to ensure that brokerage clients lose as much money as possible.

At first glance, the GCC7 offer in Malta looks like a dream role. Monday-to-Friday office hours; after the probation period, free lunches at the office and a discounted gym membership. On top of that, full training in financial markets. Pay ranges from PLN 6,500 to PLN 15,000 gross (approx. EUR 1,500–3,500) on an employment contract. As if that were not enough, the company covers flights and assists with relocation to the sunny island. GCC7 listings on Polish job portals are illustrated with images of young people enjoying life in sun-soaked Malta, in a party-like atmosphere.

“Don’t wait – send your CV today and start a new professional adventure in the heart of a Mediterranean paradise!” urges one ad.

XYZ has been contacted by individuals who were lured by this attractive offer. They told us what really lies behind it. Our reporter also set out to examine how the investment platform at the end of this story actually operates.

PLN 15,000 gross, no experience – on sunny Malta for “financial education”

According to its description, GCC7 Services is “a multicultural company that has been developing on the Maltese market for over 13 years.” It specializes in “acquiring and servicing clients in the financial sector, with a focus on online trading.” What does the job itself involve? “Active telephone advisory services for clients,” “the sale of financial services, including financial education training,” as well as “building relationships and acquiring clients for key partners.”

Although clients are meant to be educated in finance, GCC7 does not require prior experience from candidates. Job ads mention only the need for commitment and a willingness to learn. As stated, a relevant educational background is welcome – much like experience in telesales.

The company also provides full training in financial markets. Yet, according to XYZ’s source, it lasts only a few days. After that, the employee is effectively “thrown in at the deep end,” independently “educating” brokerage clients.

GCC7 assures candidates that sales targets are realistic and that commissions rise once they are exceeded. Pay ranges from PLN 6,000 to PLN 15,000 gross (approx. EUR 1,400–3,500) under an employment contract. In addition, the company offers reimbursement of flight costs after three months, initial accommodation, and relocation support. After the probation period, employees can expect not only free lunches but also, for instance, housing subsidies.

An XYZ informant – who asked to remain anonymous – admits the offer seemed attractive enough to justify relocating. On arrival, during the first few days, everything appeared exactly as advertised.

“At the beginning, I had no suspicions. The initial training sessions were genuinely good. Looking back, I think they make a real effort not to discourage new hires in those first days. Staff turnover there is enormous,” the source recalls.

“The goal is to make brokerage clients lose as much money as possible”

XYZ’s source worked at GCC7 only through the probation period. The first suspicions arose when he noticed a message on a colleague’s screen: “let’s push down the margins.” Lowering margins increases the client’s risk exposure. It also raises the likelihood that the client will be forced to top up funds to maintain their position.

As the source recounts, GCC7 employees receive bonuses tied to the size of client deposits. If a client withdraws funds, employees lose the bonus linked to that deposit.

“They openly manipulate these clients. The point is simply to make people lose as much money as possible on the platform,” the source says.

His account carries particular weight, as he himself was part of GCC7’s Polish team. Yet similar opinions can also be found online.

“This is an organized criminal group. They have robbed a lot of people. I’m warning you,” one internet user wrote under a post on the Facebook profile of a Polish classifieds portal that had boasted about a successful recruitment campaign for GCC7. Comparable comments also appear in Google reviews of the company.

“I am seriously warning you. It’s a trap,” reads one of the most frequently displayed reviews.

Names change, the scheme stays the same

The account given by XYZ’s source points to an operating model in which the GCC7 call center – servicing brands such as BrainTrade and Edutrading – acquires clients for brokers working along very similar lines, including Finansero and Tradit. Both operate on the Xcite platform.

As we have established, a comparable model had previously been described by clients of Fortissio. The activities of that broker were suspended in Poland at the end of 2025.

“The whole game is about making the client lose their initial deposit as quickly as possible so they will pay in another one. That’s why they are encouraged to open as many trades as possible,” the source explains.

In essence, the objective is for the client to lose the funds they have deposited as quickly as possible, prompting further deposits. To that end, they are pushed to open as many transactions as possible.

What can a random hire know about cocoa prices?

XYZ’s source left GCC7 before he himself began “advising” clients in a way that – he claims – would have led to losses on their side.

“Day by day, I had growing doubts whether what we were doing could be called anything other than plain money extraction,” the source says.

As he recounts, some advisers do have a background in finance. More often, however, they are people like him – effectively off the street – who, after just a few days of training, begin contacting clients and suggesting specific market actions. Formally, however, this is not classified as investment advice.

“You’re not allowed to say we are financial advisers. It is emphasized that the final decision always rests with the client. There are even penalties if someone states something outright in the form of a recommendation,” the source explains.

A legendary investor on cocoa prices

You don’t need to know anything about cocoa prices

In investing, you have thousands of opportunities every day, and prices change constantly. You don’t have to make a decision on that basis at all. No one is forcing you to do anything.

In baseball, you get three strikes – and you have to swing, or you’re out. In investing, you stand at the plate and the balls keep coming at you endlessly. You don’t have to swing at any of them to stay in the game. Eventually, when you see an opportunity you truly understand, you can choose to take a swing.”

In practice, the source says, these conversations often amount to highly assertive investment suggestions.

“We call a client and say that gold is rising or cocoa is falling, implying it’s a good time to buy. But what could someone like me really know about whether cocoa will go up or down?” he asks.

He adds that he himself began encouraging clients to take a more cautious approach to investing. While no one explicitly told him to stop, he is convinced such an attitude would not have allowed him to last long at the company. In his final days, he says, pressure also came from a supervisor referred to as a “coach.” In his view, pushing clients toward losses is built into the system.

“The Italian team even had a chart on the wall showing how it works: the average margin on a client’s account should fall, prompting the client to make another deposit. Then the margin drops again, and once more there’s a need to top up. And so it goes, over and over,” the source recounts.

If he were to point to any positive element of the training, he mentions one: during the course, employees were told to strongly discourage clients from taking out loans to invest. In practice, however – as XYZ’s reporter found – this standard may not always be upheld.

I became a BrainTrade client

The source provided contact details for another individual who had reportedly worked at GCC7 at the same time. According to him, that person, too, had misgivings. However, when approached, they reacted aggressively. Several other individuals – both employees and people claiming to have been affected – ultimately declined to speak with XYZ. Call-center staff reportedly refer to clients as “freshies”. To verify the account, I decided to become one myself and approached BrainTrade as a prospective client.

A consultant called quickly. He explained that the cheapest “education package” costs USD 200, but that I could receive it for free. There was one condition: I had to deposit money with a broker that allows the account to be linked with BrainTrade. As he put it, this involves sharing data on activity within the investment account. According to him, BrainTrade later uses this data to develop its own analytical tools. This allows consultants to see the level of security on a client’s account and what operations they are carrying out. The adviser also helped me set up an account with a broker.

When I refused to deposit funds before completing document verification, he eventually lost patience. He raised his voice and insisted that verification was not possible without a prior deposit. I stood my ground. In the end, I was given a phone contact for the Tradit helpline, which did indeed speed up the verification process. The BrainTrade consultant also offered assistance in completing the mandatory investment knowledge test, suggesting sample answers.

My BrainTrade adviser was not telling the truth

After making the minimum deposit – USD 200 – which enabled access to the “free consultations,” another consultant began contacting me. He introduced himself as someone with many years of experience in financial markets, claiming to have worked in the industry for 14 years.

The Tradit platform, however, does not allow clients to make low-risk investments. For example, gold could only be traded with leverage of at least 20x. A similar minimum leverage applied to investments in the Nasdaq index. For other commodities, the minimum leverage was around 10x; for equities, 5x; and for cryptocurrencies, 2x.

Good to know

Leverage amplifies volatility and risk

Financial leverage is a mechanism that allows investors to trade amounts larger than their own capital by using funds borrowed from a broker (for example, with 1:10 leverage, an investor can open a position ten times the size of their own deposit). While this can increase potential profits, it also significantly raises the risk of losses. When the capital is no longer sufficient to maintain a position, the investor must add funds or the position is closed at a loss.

As I was told by a BrainTrade call-center adviser, this is the so-called “EU leverage.” According to him, all brokers offering CFDs in the European Union operate with these parameters. The conversation gave the impression that even if a broker wanted to, it could not allow less risky forms of investing – supposedly because of EU regulations.

This is not true. CFDs can also be traded without the use of financial leverage (1:1). Such an option is offered to clients by, among others, some brokers operating on the Polish market.

He told XYZ

Tomasz Ciąpała: I never use leverage

Why? Because I am not a professional investor, but an entrepreneur. I do not have the time to follow stock market movements on an ongoing basis. Meanwhile, it happens that share prices can fall by as much as 30% in a single day. LPP – a stable company from the WIG20 – lost more than a third of its value overnight after the well-known Hindenburg report. The market volatility we have seen in recent years is not going away anytime soon.

With high leverage, you can wipe out your position in moments. When I invest without leverage, at worst I am left with shares that may recover over the long term. Leverage is a tool for traders – and I simply do not have the time for that. Aggressive trading is not my style either. Paraphrasing Warren Buffett: capital flows from the active and impatient to the patient.”

Does protection against loss make profits harder?

A BrainTrade call-center employee suggested, among other things, that I should avoid using stop-loss orders. A stop loss allows investors to set a level of loss at which a position is automatically closed. According to my interlocutor, however, such protection may cause an investor to miss a potential rebound in price.

A similar situation, he argued, can occur when an investor runs out of funds to maintain a position. Capital, as he put it, works “like fuel in a car.”

“If you don’t have enough money – fuel – you won’t reach your destination,” the BrainTrade employee said.

By his logic, despite the costs of holding a position overnight, it often makes sense to keep a losing investment open longer to give it a chance to recover. Remaining capital should then be used to “defend” the position - “to let it all breathe a bit,” as he explained.

“If someone has sufficient margin, they don’t worry about short-term price moves. They just wait,” the call-center employee said.

This line of reasoning, however, raised my doubts. I asked what would happen if, for example, gold kept falling for a prolonged period – say, for 100 consecutive days. I was told that in such a case the investor could simply buy more at a lower price. One could also, as he put it, “maximize profits” through “pyramiding,” that is, adding further positions.

“There hasn’t been a situation where gold didn’t rise over five years. There was one year that ended in the red,” the BrainTrade employee said.

I decided to challenge this claim.

“When gold reached around USD 1,900 per ounce in 2012, it only returned to a similar level in 2020,” I noted, referring to a price chart.

“That was during a crisis – I skipped that,” the employee replied.

“What crisis?” I asked.

From what he recalled, it was a “labor market crisis.” He added that in such situations one can always close the position and “follow the trend.” When I pressed for details about the alleged crisis, he admitted that “it was a long time ago and I don’t remember it well.”

Expert's perspective

The odds of winning with leverage are slim – closer to casino roulette

First, we need to understand the rules. Second, those rules must give us a genuine chance of winning. Third, we should be playing against participants at our level – or weaker. Much stronger opponents will defeat us quickly.

How does leveraged speculation fit into these principles? The rules may not seem particularly complex, but in reality they are full of traps. We bet on the direction in which the price of an asset will move, and the broker allows us to stake a multiple of the capital we actually have.

Suppose we have PLN 100 (approx. EUR 23) and expect the price of gold to rise. We take a position with 100x leverage. In total, we are effectively staking PLN 10,000 (approx. EUR 2,300), of which PLN 9,900 is borrowed. If the price of gold rises by 1%, we earn PLN 100 (approx. EUR 23), from which we must still deduct often substantial holding costs. If, however, the price falls by 1%, the position is liquidated and our entire capital is wiped out.

If we understand the math behind such a trade, it becomes clear that our chances of success are slim. They depend largely on short-term, hard-to-predict price movements. In practice, the odds resemble those of roulette in a casino. We are automatically at a disadvantage due to the cost of maintaining the position. We are also competing against far better-informed players who track the market continuously. Our chances are roughly those of a sailor trying to cross the Atlantic in a homemade paper boat.

My experience with BrainTrade ended before it really began

My story with BrainTrade was over before it truly began. I quickly withdrew my funds from the broker’s account. My final conversation – once I had already made that decision – took place just before the U.S. invasion of Iraq. Had I followed the suggestion and opened an oil contract, I might, by sheer luck, have ended up with a sizable profit after the weekend.

Life savings wiped out

In Poland, however, there are individuals who claim to have lost their life savings in this way. They accuse brokers operating on the Xcite platform – allegedly with the involvement of call-center staff offering “financial education” – of leading them to significant financial losses.

While I was using BrainTrade’s educational service, I managed to get in touch with someone who considers himself a victim of Edutrading and Tradit.

“It’s all a fabrication. The charts are manipulated behind the scenes,” says my second source, who also wishes to remain anonymous and is currently negotiating in an attempt to recover at least part of the lost funds.

He encountered Edutrading’s “financial education” by chance, after receiving a call from a consultant. Over time, he deposited increasingly large sums into the broker’s account. In total, he claims to have lost more than PLN 200,000 (approx. EUR 46,000) on investments linked to this “financial education.”

“They robbed me – and many others,” the source says.

After losing his life savings, an Edutrading employee told him: “Play it gently, let it grow”

As he says, he reached these conclusions after speaking with others who had lost large sums in a similar way. He mentions, among others, a woman from Gdańsk who – beyond losing her savings – allegedly paid for contact with telephone-based “financial education” with a deterioration in her health. To support his claims, the XYZ source shared recordings of conversations with the Edutrading helpline. He began recording some of them after, having lost a significant amount of money, he found himself in a state of desperation.

At that point, another Edutrading employee was “assigned” to him – presented as someone who would succeed where the previous consultant had failed. In the recordings, the call-center employee repeatedly encourages him to deposit more money into the account. She is not deterred by his admission that he has already lost all his savings. She even suggests he could try to earn additional funds or borrow money from someone.

She justifies this by pointing to what she describes as an emerging investment opportunity linked to news about new jobs in the United States. After he tells her he has lost everything, she also advises him to “play it gently, let it grow.” When, following her suggestion, he logs into the broker’s account, she asks whether they should “push the direction down or up.”

Expert's perspective

A loss of funds alone is not fraud. What can those who feel misled do?

At the same time, the internet is rife with advertisements promising quick and easy recovery of funds from brokers. Unfortunately, a significant portion of these offers are scams – yet many people still fall for them. As a result, brokers are flooded with repetitive and often unfounded complaints. This, in turn, makes it much harder today than it was five or ten years ago to pursue genuinely justified claims through complaint procedures or amicable settlement.

In practice, each case requires an individual assessment: gathering evidence, evaluating it in light of applicable regulations, identifying possible legal steps, and realistically assessing the risks and costs of further action. If the loss is not substantial, and the client still believes their claim is valid after exhausting the complaint process, they may turn to the Financial Ombudsman for a review.

In my experience, however, such proceedings are often used by brokers to drag out cases and lead to the expiration of claims. The Financial Ombudsman lacks both the staffing resources and the authority to issue binding decisions between the parties; it can only provide a non-binding legal opinion. That said, there are also cases in which the institution’s intervention genuinely helps clients.

Before Tradit and Finansero, Fortissio clients raised similar complaints

XYZ’s source has no doubt that Edutrading and BrainTrade are, in practice, the same operation under different names, with a single entity behind them. A GCC7 employee we spoke to expressed a similar view. Information available on company websites, however, indicates that Edutrading is a brand owned by Adlegion, while BrainTrade belongs to BT Nexus.

Not only do the names of “financial education” providers change – so do the brokers. Before the emergence of Malta-regulated Tradit (IFH Capital Trader) and Cyprus-regulated Finansero (Global Trade CIF), Polish clients were encouraged to invest via Fortissio. That broker – also operating on Xcite software – functioned under Greek regulation through the company Vie Finance.

Fortissio, whose activities toward Polish clients were the subject of a report by the TV program Uwaga TVN in June 2025, has, among other things, been fined EUR 37,000 by the Greek equivalent of Poland’s financial regulator in December 2025. Civil proceedings involving Polish clients are also ongoing in connection with the broker’s operations. The Greek capital markets supervisor has likewise suspended the cross-border provision of brokerage services in Poland by VIE Finance A.E.P.E.Y S.A. (Vie Finance).

“In the case of Fortissio alone, in matters where we represent affected clients before Polish civil courts, orders have already been issued – at my request – to freeze Fortissio’s bank accounts in Greek banks in the amount of EUR 470,000,” XYZ was told by attorney Patryk Przeździecki.

The regulator acted decisively… Four years after the first report

In his view, regulatory authorities often respond with delay to signals of market irregularities. He bases this assessment on more than a decade of experience handling similar cases. As he emphasizes, the first reports of potential misconduct by Fortissio reached regulators at least as early as the summer of 2021. Yet it was only on July 1, 2025 – nearly four years later – that the company was barred from providing services in Poland.

“We are currently analyzing the merits of bringing claims against the State Treasury – the Polish Financial Supervision Authority (KNF) – in individual cases where clients may have suffered losses due to potential supervisory failings by the regulator in relation to Fortissio,” says attorney Patryk Przeździecki.

The Polish Financial Supervision Authority has already warned about Edutrading

In the case of Edutrading, there is already a warning issued by Poland’s Financial Supervision Authority (KNF) in October 2025. The KNF noted that it suspected the entity of conducting brokerage or investment activities without the required license (Article 178 of the Act on Trading in Financial Instruments). Relevant provisions – Articles 69 and 79 – cover, among other things, unauthorized provision of investment services, breaches of information obligations, and operating without regulatory oversight.

XYZ has established that the Warsaw-Mokotów District Prosecutor’s Office has opened an investigation into Edutrading under Article 286 §1 of the Penal Code in conjunction with Article 294 §1.

“The proceedings are at the preliminary stage, meaning we are examining the circumstances of the act. Evidence is being collected, including the questioning of victims,” says Piotr A. Skiba, spokesperson for the Warsaw District Prosecutor’s Office.

Regarding the activities of Finansero and Tradit, we requested comments from the regulators in Cyprus and Malta. So far, only the Maltese regulator has responded, stating that it “cannot disclose, discuss, or comment on detailed information regarding actions taken beyond those that have already been explicitly made public.”

“People are dumb,” yet the BrainTrade phones keep ringing

The company behind the Xcite platform – Tiebreak Solutions, originating in Bulgaria and operating from Cyprus – presents itself as a software provider. It also claims not to provide financial services itself, noting that its technology is used by “external brokers.” However, Tiebreak Solutions did not respond directly to XYZ’s questions.

GCC7, Finansero, and Tradit also declined to comment on the allegations described in this report. Ahead of publication, XYZ was able to contact a former GCC7 employee.

“I worked at GCC7 several years ago, back when it was the Fortissio platform,” says the former employee. He notes that there are thousands of firms like GCC7, exploiting human stupidity, naivety, and greed.

“And since people are dumb and fall for some shady company? That’s on them,” he observes.

In his view, it’s normal for every salesperson to take a share of whatever the client leaves behind. Margin reduction?

“Funny. It’s not needed at all. Anyone who has no clue about CFDs [contracts for difference] will lose the money they put in, no matter where. It’s a casino, not investing,” the former GCC7 employee says.

He adds that if someone really knew how to profit from it, they could quickly become a millionaire, then a billionaire – until the world simply ran out of money. They wouldn’t even need to persuade others to invest. Meanwhile, GCC7 continues to recruit for its Polish team in Malta, and BrainTrade consultants – XYZ has confirmed – are still calling potential clients.

Key Takeaways

- At the same time, regulators had already flagged irregularities connected with entities using the Xcite platform. Poland’s Financial Supervision Authority (KNF) issued a warning regarding Edutrading, while the Greek regulator imposed penalties on Fortissio. Numerous civil lawsuits involving Polish clients are also ongoing in relation to Fortissio.

- The job offer at GCC7 may appear too good to be true. Accounts from a former employee and clients suggest practices that bear little resemblance to the advertised “financial education.” From their perspective, the actual business model may be designed to generate losses for clients – through entities united by a common denominator: all operate on the Xcite platform.

- While the individual brands share similarities, they are controlled by separate companies registered in different jurisdictions, often including so-called tax havens. Such a structure can, in itself, hinder effective regulatory oversight. As one lawyer specializing in these cases told XYZ, supervisory bodies frequently react with delay.